Chinese equities have lost more than a third (35.5%) of their value this year as investors have fretted over the country's continued lockdowns, real estate problems and strict technology regulation. With China representing over a quarter (27%) of its weight, this has dragged the EM index down 18.8%, compared to a fall of 8.0% for developed markets[1]. SKAGEN Kon-Tiki (-18.7%) is slightly ahead of the index and despite this year's challenges has delivered healthy annualised returns of 9.4% over the past two decades, 3.1% more each year on average than the benchmark.

Strong stock picking offsets Russian write-downs

One bright spot this year has been energy – the only sector of the equity market to have delivered positive returns. This has been beneficial for Kon-Tiki which has around a fifth (19.7%) of its assets in energy companies (compared to 5.7% for the index). China National Offshore Oil Corporation (CNOOC) is the fund's best performer year-to-date, while TotalEnergies is also in the top five. Other notable positive contributors are Turquoise Hill Resources (the Canadian miner received a bid from controlling shareholder Rio Tinto) and Assai Atacadista (the Brazilian food distributor has delivered strong operational performance).

Alongside CNOOC, good stock selection has softened the impact of China's equity market weakness on fund performance, with China Mobile also delivering positive absolute returns. On average, Kon-Tiki's nine Chinese holdings have outperformed broader EM equities and comfortably beaten the Chinese index, demonstrating how good stock picking can add value even in a challenging market[2].

The majority of SKAGEN Kon-Tiki's negative return this year is attributable to its five Russian holdings which made up around 10% of assets at the start of 2022 but were written down to zero following the invasion of Ukraine. One is X5 Retail Group, which is held via depositary receipts listed on the London Stock Exchange. Trading in these has recently began off-market, leading to a positive revaluation of the position.

Half-price portfolio

SKAGEN Kon-Tiki's portfolio is geographically diversified with 62% of assets listed in Asia, 16% in Latin and South America, 9% in Africa and 13% in companies listed in developed markets but with EM exposure. The fund's other significant overweight positions versus the index are South Korea (24% of assets vs. 12% of the benchmark), Brazil (14% vs. 6%) while it is underweight India (4% vs. 16%). The portfolio is also tilted more towards smaller companies with 20% of assets in small and mid-cap stocks compared to 10% of the index.

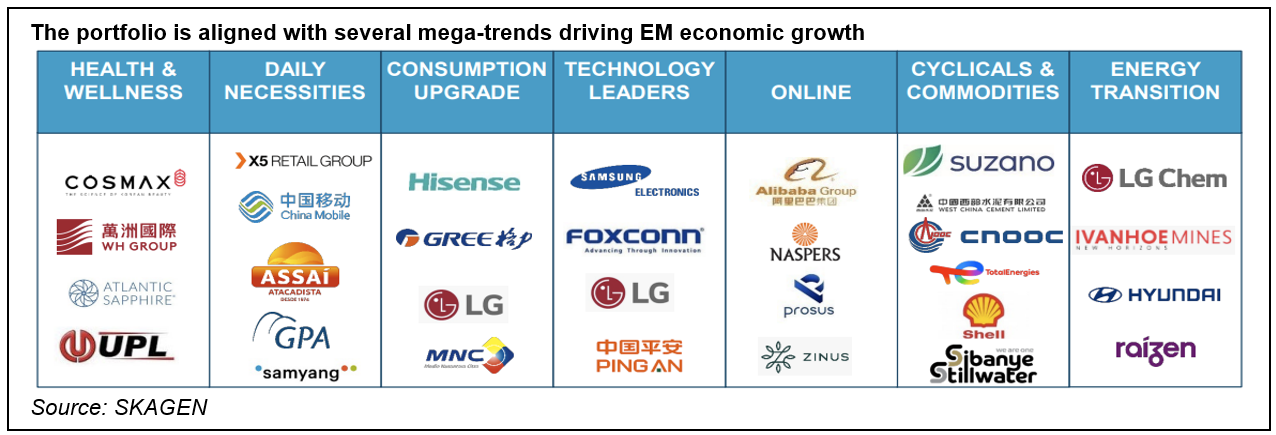

The fund is almost 50% cheaper than the EM market on both a P/E and P/B basis[3] with estimated upside of 83% over the next 2-3 years. Despite the portfolio's value focus, its holdings contribute towards (and benefit from) many of the secular drivers of EM growth with developing economies expected to significantly outpace advanced ones this year and next according to the IMF's most recent World Economic Outlook[4]. The portfolio's quality is also reflected in its return on equity – a measure of profitability – being on a par with that of the benchmark, despite trading at half its valuation[5].

Diversification key to navigate uncertain outlook

With the economic outlook remaining uncertain, the portfolio is positioned to weather different growth and inflationary environments. The fund is expected to perform slightly better in a scenario of higher inflation and lower growth, which is aligned with the majority of economic forecasts, but holdings should also perform strongly if we see a more positive 'Goldilocks scenario' with stable growth and lower price rises.

The outlook is also clouded by geopolitical uncertainty, notably around Russia and China. This creates added risks for investors but also opportunities. The Chinese equity risk premium, for example, is currently 9% – as high as it has been since the global financial crisis a level which has historically nearly always rewarded brave investors with positive absolute returns[6].

Another positive is that despite the outperformance of traditional value sectors like energy, financials and basic materials over the past two years, EM value still trades near historical lows versus EM growth on both a P/E and P/B basis. This offers good down-side protection but also the potential for significant rewards ahead – despite 2022 being turbulent and the outlook uncertain, valuation remains a reliable guide to future long-term returns.

All figures as at 31/10/2022 unless stated.

[1] As at 31/10/22. MSCI Emerging Markets Index -18.8%, MSCI World Index -8.0%. All figures in EUR.

[2] YTD NOK returns at 31/10/22: Kon-Tiki -16.7%, MSCI EM Index -16.8%, Kon-Tiki China -11.2%, MSCI China Index -32.7%.

[3] P/E (22e) 5.3x Kon-Tiki vs. 10.3x Index; P/B 0.7x Kon-Tiki vs. 1.3x Index (Kon-Tiki valuations for top 35 holdings).

[4] Source: International Monetary Fund, World Economic Outlook, October 2022

[5] Trailing 12-month ROE: Kon-Tiki 13.1% (weighted top 35 holdings) vs. MSCI EM Index 13.5%

[6] Equity risk premium defined as China Index expected earnings yield - 10-year Chinese government bond yield.